Middle East Production Offline: Current Status, Restart Timelines, and Well Damage Risk

March 30, 2026 Strait of Hormuz: Effectively closed since March 1, 2026 (29 days)

More crude oil is offline right now across the Middle East than at any point in the history of the global oil market. What the data shows about the actual restart timeline, the physical infrastructure that has been permanently destroyed, and the well damage compounding under the surface right now should change how you think about this crisis. The market is pricing a light switch. The production math says otherwise.

Part 1: Current Middle East Production Offline

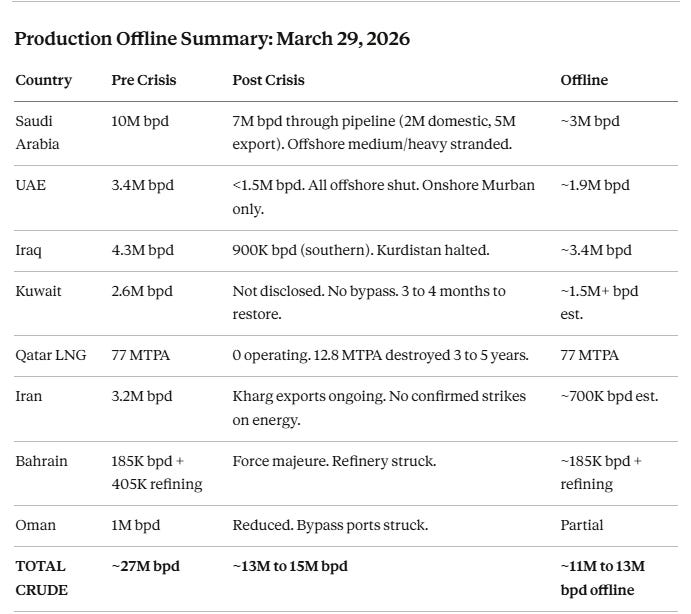

The Strait of Hormuz has been effectively closed for 29 days. Approximately 11 to 13 million bpd of crude production is now offline across the region, with 77 MTPA of LNG (20% of global trade) at zero. Pre crisis, roughly 20 million bpd of petroleum transited Hormuz.

Below is the country by country breakdown.

Saudi Arabia (Saudi Aramco)

Pre-crisis production: ~10 million bpd (Q4 2025 OPEC data) Current estimated production: ~7 million bpd through East West pipeline to Yanbu (2 million domestic, ~5 million net export). Offshore medium and heavy crude stranded. March exports: 4.355 million bpd, down from 7.108 million in February (39% decline) Offline: ~3 million bpd

What Aramco has said directly:

CEO Amin Nasser (March 10 earnings call): The East West pipeline to Yanbu was carrying 2.8 million bpd before the war and has reached its full 7 million bpd capacity. Approximately 2 million bpd serves domestic refining. Net export via Yanbu is approximately 5 million bpd.

Aramco is focusing on lower cost onshore fields producing light and extra light crude. Medium and heavy crude from offshore fields is stranded.

Aramco began cutting output at two unnamed oilfields as of March 9.

Aramco cut crude supply allocations to Asian buyers in April for the second consecutive month.

Infrastructure impact:

Ras Tanura refinery (550,000 bpd) shut after drone interception on March 2. Minor damage, remains offline.

A drone crashed into the SAMREF refinery at Yanbu, briefly interrupting Red Sea loadings. This is the first confirmed strike on Saudi bypass infrastructure.

Strategic response: Saudi Arabia is the only major Gulf producer with meaningful bypass infrastructure. The East West pipeline gives the Kingdom the ability to move up to 7 million bpd to Red Sea terminals, but ~2 million of that serves domestic needs. Net export capacity of ~5 million bpd falls short of pre crisis export volumes. The grades that remain constrained are medium and heavy crude from offshore fields, which are not suited to pipeline transport.

United Arab Emirates (ADNOC)

Pre-crisis production: ~3.4 million bpd Current estimated production: Less than 1.5 million bpd. All offshore shut. Onshore Murban only. Offline: ~1.9 million bpd

What ADNOC has said directly:

ADNOC stated it is “actively managing offshore production levels to address storage requirements” while onshore operations continue (March 7).

All offshore production shut. ADNOC released its Murban Crude Oil Availability Forecast on March 27, deferring planned onshore maintenance from May to September to maximize Murban output.

ADNOC Gas confirmed core processing unaffected, LNG production adjusted (March 24).

What is offline by field (Kpler vessel-tracking data):

Upper Zakum: Over 1 million bpd (offshore, shut)

Das Blend: Nearly 700,000 bpd (offshore, shut)

Umm Lulu: ~230,000 bpd (offshore, shut)

Onshore Murban crude: Was exporting ~1.5 million bpd in February (increased from 1.135 million bpd in January). Some onshore operations continuing.

Infrastructure damage:

Ruwais Refinery 2 (West): 417,000 bpd crude distillation unit shut after drone strike on March 11. ADNOC planning plant-wide safety shutdown.

Ruwais Refinery 1 (East): 400,000 bpd facility had already reduced operations 10 to 20% on March 6.

Combined Ruwais complex can refine 922,000 bpd and serves as central hub for downstream operations (chemicals, fertilizer, industrial gas).

Mussafah fuel terminal (Abu Dhabi): Fire from drone strike.

Jebel Ali port (Dubai): Fire from drone interception debris.

Fujairah port: Oil loading operations suspended multiple times after drone attacks. Operations suspended again March 16.

Bypass capacity: ADNOC operates a 1.5 million bpd pipeline to Fujairah on the UAE’s eastern coast (Gulf of Oman side), which can bypass Hormuz. However, Fujairah itself has been attacked, complicating this alternative. The UAE ships only 66% of exports through Hormuz (vs. 100% for Kuwait, Qatar, and effectively Iraq), giving it more flexibility than its neighbors.

Iraq (Ministry of Oil / Basra Oil Company)

Pre-crisis production: ~4.3 million bpd Current estimated production: 900,000 bpd (southern fields, reduced from 3.3 million). Kurdistan (~200K bpd) also halted. Offline: ~3.4 million bpd Iraq is the hardest hit producer.

What Iraqi officials have said directly:

Deputy Oil Minister Hayan Abdul Ghani confirmed on March 27 that Basra Oil Company output has been reduced from 3.3 million bpd to 900,000 barrels. Current output directed toward domestic refineries.

Deputy Oil Minister for Extraction Bassem Mohammed Khudair stated on March 27 that “most activities and projects are currently suspended due to the reality imposed by the war.” He said production could return to previous rates “within days if the crisis ends.”

Basra Oil Company sent official letters to BP (March 24) requesting North Rumaila be cut to 350,000 bpd from 450,000, citing “high and critical levels at its storage depots.” Similar letter sent to Eni requesting 70,000 bpd cut from Zubair.

Force majeure declared on foreign oil company operations.

Shutdown sequence (from MEED reporting on internal Iraqi documents): Iraq executed a four-part emergency shutdown plan:

First fields shut: March 3

Rumaila (Iraq’s largest, world’s second-largest field) fully suspended March 3 at 15:00 local time. Rumaila alone represents roughly 36% of Iraq’s output.

West Qurna 2 also shut.

Phase 4 fully implemented March 4. Internal correspondence noted: “in the event that heavy crude exports completely stop, Maysan fields will be fully shut down.”

North Rumaila and Zubair fields were initially kept running to maintain gas processing rates.

Storage situation at time of shutdown:

Total oil storage capacity: 6,350 thousand barrels

Available space: 3,700 thousand barrels nameplate, but 1,300 thousand barrels at Tuba could not be used because it could collapse receiving jetties.

Effective available storage: approximately 2,400 thousand barrels. At pre-crisis production of 4.3 million bpd, that filled within days.

Infrastructure damage:

Majnoon oilfield attacked (already suspended, struck again).

Oil port operations at Basra suspended March 12 after two tankers carrying fuel were hit in Iraqi territorial waters by Iranian explosive-laden boats.

Iraqi Kurdistan: Production halted by DNO, Gulf Keystone, Dana Gas, HKN Energy (~200,000 bpd). Ceyhan pipeline exports to Turkey also suspended.

Northern alternative route: Iraq’s Oil Ministry sent a letter to the KRG requesting at least 100,000 bpd of crude be pumped from Kirkuk fields through the Iraq-Turkey pipeline to Ceyhan. This pipeline has 1.2 million bpd capacity but requires a political agreement between Baghdad and Erbil that has not been reached. Even if it were, diverting Kirkuk crude for export risks depriving northern Iraq’s refineries and power plants of feedstock.

Fiscal exposure: Oil provides 90% of government revenue. Monthly oil receipts averaged slightly over $6 billion. Each week of closure cuts export proceeds by approximately 0.4% of GDP (Fitch Ratings). Iraq’s international reserves stood at $97.5 billion as of November 2025.

Kuwait (KPC / Kuwait Oil Company)

Pre-crisis production: ~2.6 million bpd (February 2026) Current estimated production: Not disclosed. Force majeure in effect since March 7. Offline: ~1.5M+ bpd estimated

KPC CEO Sheikh Nawaf Al-Sabah stated at CERAWeek on March 24 that KPC was “forced” to reduce crude oil production due to disruptions to free navigation in the Strait of Hormuz. He said attacks on oil refineries in Kuwait were “utterly unprovoked” and that “there is no alternative to the Strait of Hormuz.” Alternative pipelines and strategic reserves “don’t represent even an iota of normal export flows.” KPC expects to restore production to full capacity in 3 to 4 months once the war ends.

Mina Al-Ahmadi refinery hit by drone attacks, fire in several units. Kuwait International Airport fuel tank hit by drones.

Critical vulnerability: Kuwait ships 100% of its crude exports through Hormuz and has no major bypass pipeline.

Qatar (QatarEnergy)

Pre-crisis capacity: 14 LNG trains, 77 million tonnes per year. Approximately 20% of global LNG trade. Current status: All LNG production halted. 12.8 MTPA physically destroyed. Force majeure declared March 4.

QatarEnergy CEO Saad Al-Kaabi confirmed that missile strikes on March 18 and 19 physically damaged two LNG trains at Ras Laffan. Trains 4 and 6 totaling 12.8 million tonnes per year of capacity, approximately 17% of Qatar’s exports. Al-Kaabi stated the damage will take 3 to 5 years to repair, with an estimated $20 billion per year in lost revenue. Force majeure declared on specific long term contracts with Italy, Belgium, South Korea, and China.

The initial shutdown (March 2) was precautionary after drone strikes that caused no major damage. The March 18 to 19 missile strikes converted this into physical destruction. Even if every other condition normalizes tomorrow, 12.8 MTPA of global LNG supply is gone for years. The remaining 12 undamaged trains can restart once Hormuz reopens.

Downstream production of polymers, methanol, aluminum and other products also halted since March 3.

Iran (NIOC)

Pre-crisis production: ~3.2 million bpd crude (~1.3 to 1.6 million bpd exports, primarily through Kharg Island) Current status: Oil infrastructure at Kharg Island has not been struck. Iran continues exporting crude. CENTCOM’s Operation Epic Fury targets military infrastructure, not energy. The April 6 deadline for potential strikes on energy plants is the key binary risk.

Key data (Kpler):

94% of Iran’s crude exports originated from Kharg Island over the past 12 months.

Kharg terminal storage: ~31 million barrels capacity, inventories at ~18 million barrels (58%) as of March 7.

Iran exported 13.7 million barrels since the war started. Multiple tankers were loading at Kharg as recently as March 11.

Iran’s alternative export route: Jask terminal (Gulf of Oman, outside Hormuz). Goreh-Jask pipeline designed for 1 million bpd but effective capacity closer to 300,000 bpd with historically low utilization.

Trump’s explicit threat: If Iran interferes with Strait of Hormuz shipping, oil infrastructure on Kharg will be targeted. Iran responded that oil facilities linked to U.S. companies would be reduced to “a pile of ashes.”

Bahrain (Bapco Energies)

Pre-crisis crude production: ~185,000 to 200,000 bpd (OPEC secondary sources report 174,000 bpd for 2024; projected to exceed 200,000 bpd in 2026) Refining capacity: 405,000 bpd at Sitra refinery (recently upgraded from 267,000 bpd under the multi-billion dollar Bapco Modernization Program, completed late 2025) Current status: Force majeure declared on all group operations, March 9, 2026. Sitra refinery severely disrupted.

What Bapco has said directly:

Bapco Energies declared force majeure on March 9, stating its “group operations have been affected by the ongoing regional conflict in the Middle East and the recent attack on its Refinery complex.”

The company stated “all local market needs are fully secured according to the proactive plans in place, ensuring the continuity of supplies and meeting local demand without impact.”

Bapco did not specify the extent of damage to the refinery.

Infrastructure damage:

Sitra refinery (405,000 bpd, Bahrain’s only refinery) was struck at least twice. The first attack occurred in the early days of the conflict (reported damaged the previous week). A second Iranian drone attack hit on March 9, causing thick smoke to surround the complex. Bapco had recently completed the BMP modernization that more than doubled the refinery’s capacity to 405,000 bpd from 267,000 bpd, adding higher-value product capability (jet fuel, low-sulfur diesel).

Sitra area residential neighborhoods also hit: 32 Bahraini civilians including children injured in the March 9 drone attack (Bahrain’s National Communication Center).

The 90-year-old refinery complex serves as the central hub for all of Bahrain’s downstream operations.

Production structure: Bahrain receives crude from two sources: the onshore Bahrain Field (Awali), which produces only about 33,000 bpd (down from 75,000 bpd at peak in the 1970s), and the offshore Abu Saafa field shared equally with Saudi Arabia (Bahrain’s share approximately 125,000 to 150,000 bpd). Abu Saafa produces high-quality light crude. Bahrain imports additional crude to feed its 405,000 bpd refinery, making it a net crude importer despite being a producer.

Critical vulnerability: Bahrain ships between 87% and 95% of its total exports through the Strait of Hormuz (Fitch Ratings estimate). The country has no bypass pipeline. Bahrain’s economy is heavily dependent on the refinery for both domestic fuel supply and export revenue from refined products. The recent $7 billion modernization of Sitra was designed to position Bahrain as a regional refining hub, and that investment is now at risk. Each week of closure cuts export proceeds by approximately 0.4% of GDP (Fitch).

Unique dimension: Bahrain is not just a crude producer; it is a significant refiner and product exporter. The 405,000 bpd Sitra refinery processes far more crude than Bahrain produces domestically, importing feedstock from Saudi Arabia and elsewhere. The refinery’s output (gasoline, jet fuel, diesel, LPG) serves both Bahraini domestic consumption and GCC export markets. The refinery damage therefore has a double impact: Bahrain loses both its crude export revenue and its refined product export revenue, while also threatening domestic fuel security despite Bapco’s assurances.

Oman

Pre-crisis production: ~1 million bpd Infrastructure damage: Duqm port struck. Oil export terminal in Oman hit by drone strikes (reported March 14). Oman ships a smaller share through Hormuz than its neighbors.

Regional Refining Capacity Offline

IIR Energy estimates refineries in Saudi Arabia, Iraq, UAE, Bahrain, Kuwait, and Qatar have shut roughly 1.9 million bpd of crude refining capacity. The IEA puts it higher: more than 3 million bpd of refining capacity in the region has shut due to attacks and lack of viable export outlets.

Part 2: Production Restart Timelines

The question is not just “when does Hormuz reopen” but how long it takes to bring production back to pre-crisis levels once it does. These are fundamentally different timelines. The strait reopening means tankers can move. But restarting millions of barrels of shut-in production across dozens of fields with different geological characteristics is an engineering problem that compounds with every week of shutdown.

If Hormuz Opens Today (29 days of shutdown)

Timeline to full production: 8 to 14 weeks

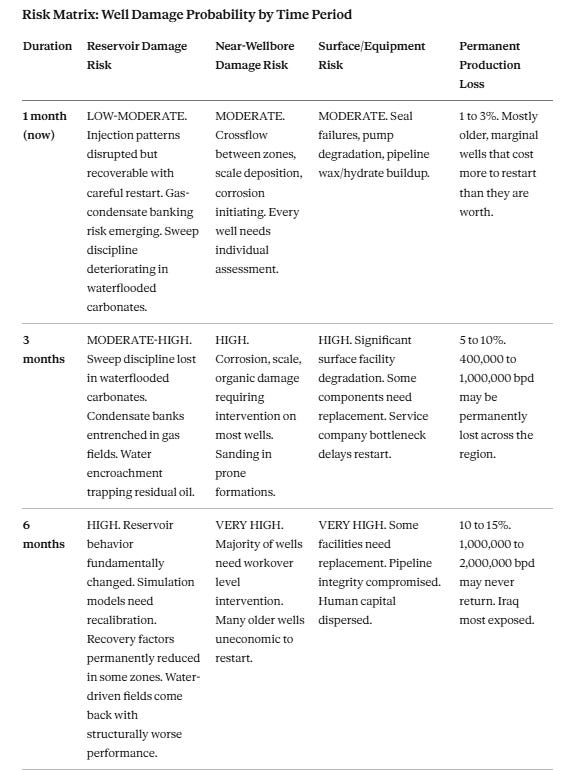

At 29 days, the shutdown has crossed into the 1 month threshold. The subsurface is no longer in the “relatively low damage” window. Waterflooded carbonates across Iraq and the UAE are losing sweep discipline. Near wellbore damage is accumulating. This is no longer just a logistics restart.

What has to happen before barrels flow:

Insurance and tanker repositioning: War risk insurance must be restored. Over 150 tankers were stranded outside the strait. P&I clubs pulled coverage effective March 5. Getting insurance reinstated and tankers repositioned takes 1 to 2 weeks minimum.

Well by well restart sequence: Each well needs pressure buildup verification, choke management, monitoring of gas to oil ratio transients. Fields cannot simply be turned back on at full rate.

Injection restart before production restart: Many Middle East fields depend on water injection for pressure support. Injectors must restart and stabilize before producers come back, or you get distorted flood fronts and premature water breakthrough.

Surface facility integrity check: Static equipment that has been sitting idle for a month needs inspection. Wax, asphaltene, sand, and hydrate risk in flowlines has accumulated.

Gas processing restart: Many fields co produce gas that feeds power generation and domestic consumption. The sequencing of gas processing restart affects everything downstream.

Service company mobilization bottleneck: Every country needs the same workover crews simultaneously. This creates a queue that extends the timeline.

Country specific restart at Day 29:

Saudi Arabia: Best positioned. East West pipeline already at capacity, onshore light crude flowing. 60% within 2 weeks, 90% within 6 weeks, full restoration 8 to 10 weeks.

UAE: Offshore restart is the binding constraint. ADNOC deferred maintenance to maximize Murban. 40 to 50% within 2 weeks, 80% within 6 weeks, full restoration 8 to 10 weeks.

Iraq: Deepest cuts (79%), weakest institutional capacity. Rumaila shut 26 days. 25 to 35% within 2 weeks, 60% within 6 weeks, full restoration 10 to 14 weeks. Some marginal wells may never restart.

Kuwait: KPC CEO Al-Sabah stated 3 to 4 months to full capacity, with proportional restoration over that period. No bypass infrastructure.

Qatar LNG: Undamaged trains (12 of 14) could achieve partial output 4 to 6 weeks after reopening, full restoration 10 to 14 weeks. Trains 4 and 6 are physically destroyed and offline for 3 to 5 years.

Bahrain: Crude production restart 3 to 4 weeks. Sitra refinery depends on damage extent. If limited, partial restart 4 to 6 weeks. If structural, 3 to 5 months.

If Hormuz Opens in 1 Month (approximately 48 days of shutdown)

Timeline to full production: 4 to 10 weeks after reopening

At one month, the situation shifts from “deferred barrels” to “changed subsurface behavior” in many fields.

What changes at the one-month mark:

Waterflooded carbonates (dominant geology in Iraq and UAE) lose sweep discipline. The injection-production pattern that took years to optimize does not automatically reset when you restart. Water returns through high-permeability channels. The first few days after restart may show deceptively low water cut (the cone relaxes during shutdown), followed by rapid water breakthrough.

Near-wellbore issues accumulate: organic precipitates, emulsions, scale deposition, sand settling. Every well that restarts needs individual cleanup treatment.

Sour gas assets (UAE) accumulate hydrate, corrosion, and integrity exposure.

Equipment degradation: ESPs (electric submersible pumps) are finicky after prolonged shutdown. Seals designed for steady-state operation can fail during the pressure/temperature cycling of restart.

Gas-condensate systems (Qatar North Field): Condensate dropout near the wellbore creates a liquid bank that may not fully clear even when pressure rises above dew point. Some individual wells may come back at lower deliverability permanently.

Historical reference: 2020 COVID shutdowns. During COVID, when U.S. and Canadian producers shut approximately 4.5 million bpd, the restart took months, not weeks. Data from wells shut 6 to 24 months showed an average 25% decrease in oil rate and 22% increase in water rate post-restart. But COVID shutdowns were different: the Middle East fields being shut now are mostly high-pressure, high-rate conventional systems, not depleted shale. Still, the principle that restart is harder than shutdown applies.

Estimated restart at 1 month (this is where we are now):

Saudi Arabia: 60% within 2 weeks of reopening, 90% within 6 weeks, full restoration 8 to 10 weeks.

UAE: 40 to 50% within 2 weeks, 80% within 6 weeks, full restoration 8 to 10 weeks.

Iraq: 25 to 35% within 2 weeks, 60% within 6 weeks, full restoration 10 to 14 weeks. Some older, marginal wells may never restart. Iraq has cut deeper than any producer (79% from southern fields) and has the weakest institutional capacity for coordinated restart.

Kuwait: KPC CEO Al-Sabah stated 3 to 4 months to full capacity, with proportional restoration over that period.

Qatar LNG: Undamaged trains (12 of 14) could achieve partial output 4 to 6 weeks after reopening, full restoration 10 to 14 weeks. Trains 4 and 6 are physically destroyed and offline for 3 to 5 years.

Bahrain: Crude production restart 3 to 4 weeks. Sitra refinery depends on damage extent. If limited to specific units, partial restart 4 to 6 weeks. If structural, 3 to 5 months.

If Hormuz Opens in 3 Months (approximately 108 days of shutdown)

Timeline to full production: 3 to 6 months after reopening. Some production may be permanently lost.

Three months of fieldwide shutdown enters territory with very limited historical precedent at this scale. The closest analogues are the Iranian Revolution (1978 to 1979), the Iraqi invasion of Kuwait (1990 to 1991), and the Venezuelan strike (2002 to 2003).

What changes at three months:

Loss of production and injection pattern balance becomes the dominant issue. Per the CrudeCast technical assessment: “Months-long fieldwide stops in mature waterflooded oil or condensate-rich gas assets can steepen the apparent post-restart decline even if average pressure looks better, because deliverability and sweep do not automatically reset with pressure.”

History-matched simulation models may need complete recalibration after a long fieldwide stop.

Wellbore integrity issues become serious. Corrosion from static fluid columns, tubular degradation, seal failures. Every well is essentially a workover candidate.

Sand-prone formations (Kuwait’s mature sandstones, parts of southern Iraq) face mechanical damage risk from repeated pressure cycling.

Service company mobilization bottleneck: Restarting hundreds of wells across multiple countries simultaneously requires workover rigs, coiled tubing units, chemical treatment crews, and wireline teams that simply do not exist in sufficient numbers in the region. This creates a queue that extends the restart timeline.

Historical reference: Kuwait after the 1991 Gulf War. Iraqi forces damaged approximately 700 wells, with over 600 set on fire. Despite catastrophic physical damage, Kuwait emerged with no political barriers to recovery. Firefighting and well-capping took 10 months (last well capped November 6, 1991). But the production recovery was faster than the well-capping: Kuwait exceeded pre-disruption annual production levels in less than two years. The key point: Kuwait’s 1991 damage was physical (explosives, fire), not reservoir. The rocks were fine. The current Hormuz shutdown is also not physically damaging the reservoirs, but three months of zero flow creates subsurface complications that 1991 did not.

Historical reference: Iranian Revolution (1978 to 1979). Per EIA data, the revolution resulted in an average drop of 3.9 million bpd over the 1978 to 1981 period, with initial supply loss reaching nearly 90% of total Iranian production. While some production returned within two years, Iran’s production in 2010 was still more than 1.5 million bpd below its 1977 average. But Iran’s case involved regime change, sanctions, the Iran-Iraq War, and institutional collapse. Not purely a restart problem.

Historical reference: Venezuelan strike (December 2002). Two-thirds of Venezuela’s 3.0 million bpd was disrupted. Within a year, production returned to about 85% of pre-strike levels. But Venezuela’s production has never returned to its pre-strike level. Chavez fired 18,000 PDVSA workers, destroying institutional knowledge. Again, the human capital loss mattered more than the geology.

Estimated restart at 3 months:

Saudi Arabia: 50% within 4 weeks, 80% within 3 months, 95% within 6 months. Aramco’s institutional depth and operational discipline position it for the strongest recovery of any Gulf producer. Some offshore fields may require extended workover programs (100,000 to 200,000 bpd).

UAE: 40% within 4 weeks, 70% within 3 months, 90% within 6 months. Sour gas and condensate-rich offshore fields slowest to return.

Iraq: 25 to 30% within 4 weeks, 50 to 60% within 3 months, 80% within 6 months. Some fields (particularly older, higher water-cut producers) may lose 300,000 to 500,000 bpd permanently.

Kuwait: KPC CEO stated 3 to 4 months from current state. At 3 months of total shutdown, full restoration likely extends well beyond that estimate.

Qatar LNG: 30 to 40% of undamaged trains within 6 weeks, 70% within 3 months, 90% within 6 months. Trains 4 and 6 remain offline for years.

Bahrain: Crude production recoverable within 4 to 6 weeks. Sitra refinery: at 3 months of shutdown plus physical drone damage, a full assessment and repair program is required. If damage was contained, 60 to 70% refining capacity within 3 months; if structural damage to modernized units, potentially 6 to 12 months. The compounding factor is that Bahrain imports crude to run its refinery, and those import flows depend on Hormuz reopening and tanker availability.

If Hormuz Opens in 6 Months (approximately 198 days of shutdown)

Timeline to full production: 6 to 18 months after reopening. Significant permanent production losses likely.

Six months of shutdown is unprecedented for this scale of production. No major oil producing region has ever shut down 11 to 13 million bpd for half a year and then attempted to restart.

What changes at six months:

Wells become permanent casualties. At six months of shutdown, a significant percentage of older, marginal, and complex wells will never restart economically. The cost of workover, recompletion, and stimulation exceeds their remaining value.

Reservoir damage transitions from “changed behavior” to “structural.” Water encroachment in shut-in oil zones traps residual oil at high pressures, permanently reducing recovery. Water-driven fields come back with fundamentally worse coning. Gas-condensate banks around wellbores become entrenched.

Surface infrastructure deteriorates. Pipelines, separators, and processing facilities exposed to desert heat, sand, and corrosive fluids without flow degrade faster than the same equipment operating normally. Some facilities will need replacement, not repair.

Human capital disperses. Oil field workers, engineers, and technical staff migrate to other employment. Reconstituting operational teams takes months.

Injection patterns become unrecoverable. In mature waterflooded fields, the sweep pattern built over years of careful management is gone. The field essentially needs to be re-developed, which means new injection studies, new simulation models, and new allocation strategies. This takes years.

Estimated restart at 6 months:

Saudi Arabia: 40% within 6 weeks, 70% within 6 months, 85 to 90% within 12 months. Aramco’s low-cost onshore fields and institutional depth make it the most resilient producer in a prolonged shutdown. Some offshore and complex field production (200,000 to 400,000 bpd) may require extended workover programs to fully restore.

UAE: 30% within 6 weeks, 60% within 6 months, 80 to 85% within 12 months. Permanent loss of 300,000 to 500,000 bpd.

Iraq: 20% within 6 weeks, 40% within 6 months, 65 to 75% within 12 to 18 months. Permanent loss of 500,000 to 1,000,000 bpd. Iraq’s institutional capacity is the weakest; restart will be slowest and most incomplete.

Kuwait: 35% within 6 weeks, 60% within 6 months, 80% within 12 months. Permanent loss of 200,000 to 400,000 bpd.

Qatar LNG: 20 to 30% of undamaged trains within 8 weeks, 60% within 6 months, 80 to 85% within 12 months. Trains 4 and 6 remain offline for years regardless.

Bahrain: Crude production (small volumes) recoverable within 6 to 8 weeks. Sitra refinery at 6 months of inactivity plus physical strike damage faces a potentially multi-quarter recovery. Extended idle time on a recently modernized refinery that had not yet fully optimized its new units compounds the drone damage. Full refinery restoration: 6 to 12+ months. Bahrain’s role as a regional refined product exporter may be permanently diminished if repair costs approach the original BMP investment.

Part 3: Well Damage Risk Assessment by Time Period

Risk Factors by Field Type (Middle East Specific)

1. Mature Water-Drive Sandstones (Greater Burgan/Wara in Kuwait, southern Rumaila in Iraq)

These are the most exposed to restart damage.

During shutdown: water cones relax temporarily (looks good), but at restart with aggressive drawdown, water returns through the same high-permeability channels.

Sand production risk: repeated pressure cycling aggravates sanding in weaker, unconsolidated intervals. This is a near-wellbore mechanical problem that gets worse with each pressure change.

Historical note: After the 1991 Gulf War, KOC’s reconstruction (”Al Ta’meer” phase) focused on rehabilitation of 18 damaged gathering centers and recovery of approximately 20 million barrels of weathered crude from 240 surface oil lakes. The physical infrastructure was the bottleneck, not the reservoir.

2. Waterflooded Fractured Carbonates (Iraq and UAE major fields)

Dominant geology in the region. Injection-production pattern balance is everything.

Shutdown pauses both production and injection simultaneously. On restart, the same production allocations do not automatically recreate the same flood front.

Viscous fingering, bypass, and front distortion are textbook risks in this scenario.

The deceptive restart: reservoir pressure may look healthier early on (it built up during shutdown), while flood conformance is still poor. Water returns quickly after a brief “cleaner” period.

Water chemistry issue: mixing formation water with injected water after a long pause causes scale precipitation. Adds skin damage to an already complex near-wellbore environment.

3. High-Pressure Gas-Condensate Systems (Qatar North Field)

Short shutdowns are generally more reservoir-tolerant in high-pressure gas fields.

The critical issue is dew point. If liquid condensate drops out near the wellbore, productivity falls dramatically. Some of that dropped-out condensate may remain unrecoverable even if pressure later rises above dew point.

The restart does not automatically restore deliverability in a rich-gas system.

A poor restart protocol can permanently compromise individual wells’ production rate even if the reservoir pressure is fine.

4. Sour Gas Assets (UAE)

During shutdown: accumulation of hydrate, corrosion, and integrity exposure.

Hydrogen sulfide (H2S) corrosion of tubulars accelerates in static fluid columns.

Return to plateau is delayed by integrity verification requirements before high-pressure sour gas production can resume.

The Compounding Problem

The critical insight is that well damage is not linear. It compounds. A well that sits idle for three months does not have three times the damage of a well idle for one month. The damage accelerates because:

Early in shutdown (days to weeks): gravity segregation separates fluids, pressure equilibrates across zones, organic precipitates begin forming in static columns. These are mostly reversible with proper restart procedures.

Mid-shutdown (weeks to months): crossflow between zones mixes incompatible fluids, scale precipitates in the near-wellbore, water invades gas-saturated pore space. These require active intervention (chemical treatment, stimulation, workover) but are still largely recoverable.

Late shutdown (months): corrosion compromises tubular integrity, mechanical damage from pressure cycling becomes structural, injection patterns are lost, reservoir behavior changes. Some of this is irreversible. The field comes back, but not the same field.

Extended shutdown (6+ months): the field needs to be re-developed, not just restarted. New wells may be needed to replace permanently damaged completions. Injection studies need to be re-run. This is a multi-year capital program, not an operational restart.

What the Market Is Not Pricing

The market is treating this as a temporary disruption with a light switch on the other end. That assumption dramatically underestimates the time required to bring production back once the strait is open.

Even if Hormuz reopened today, full production recovery takes 8 to 14 weeks for crude. Kuwait’s own CEO says 3 to 4 months. The market will be short 3 to 5 million bpd for weeks after reopening and 1 to 2 million bpd for months after that.

Qatar has suffered permanent physical destruction. 12.8 MTPA of LNG capacity is offline for 3 to 5 years regardless of what happens with Hormuz. The global LNG supply picture has structurally changed.

April 6 is the next binary risk event. Either negotiations produce a breakthrough or the target set expands to energy infrastructure. If the closure extends through April without resolution, the region crosses into the 3 month scenario where 5 to 10% permanent production loss becomes the baseline.

Approximately 20 million bpd of petroleum normally transited Hormuz before the crisis. With 11 to 13 million bpd of regional crude production now offline, even an optimistic restart means the market will be short millions of barrels per day for months.

Sources: Aramco CEO Amin Nasser, March 10, 2026 earnings call. ADNOC statements March 7, 24, and 27. Iraqi Deputy Oil Minister Hayan Abdul Ghani via INA, March 27. Iraqi Deputy Oil Minister for Extraction Bassem Mohammed Khudair via INA, March 27. Basra Oil Company letters to BP and Eni, March 24. Iraqi Ministry of Electricity, March 21. KPC CEO Sheikh Nawaf Al-Sabah, CERAWeek March 24 (via QNA). KPC force majeure notice, March 7. QatarEnergy CEO Saad Al-Kaabi, March 20 to 24. QatarEnergy force majeure declarations March 4 and 24. Qatar Ministry of Defence, March 2. Bapco Energies force majeure declaration, March 9. U.S. Central Command, centcom.mil. Kpler vessel tracking data. SPE shut in studies. CrudeCast reservoir engineering analysis (Cyrus Ashayeri), March 9, 2026.

Exactly the data and analysis I needed. Thanks for that great post !

Best detailed analysis I have seen to-date. Thanks Tracy.