The G-7 SPR Bluff: Why 300 to 400 Million Barrels Changes Nothing

The arithmetic of strategic reserves against a physical supply crisis that dwarfs every tool in the toolkit

The G-7 is a group of Atlantic basin countries proposing to release Atlantic basin barrels at Atlantic basin draw rates to solve a Pacific basin crisis. The arithmetic does not work even if the politics did.

300 to 400 million barrels is a number designed to move headlines for 48 hours. It is not a number designed to move molecules to where they are needed.

The G-7 is discussing a coordinated release of 300 to 400 million barrels from IEA strategic petroleum reserves to address the Hormuz supply crisis. The math makes this functionally irrelevant. IEA releases have never exceeded 2 million barrels per day. The physical production deficit is 6.2 to 6.7 million bpd with net missing flows of approximately 14 million bpd. The barrels are stored in the Atlantic basin. The crisis is in the Pacific basin. Only 3 of 7 G-7 members support the release. The IEA executive director is working against it. The probability of an actual coordinated release this week is 25% to 35%, and even if it materializes, it will be smaller than the headline number and physically incapable of reaching the markets that need it most.

A Stock Is Not a Flow

The number being floated, 300 to 400 million barrels, sounds enormous in isolation. It represents 25% to 30% of the 1.2 billion barrels IEA member countries hold in combined public emergency stocks. It would be the largest coordinated release in the IEA’s 52 year history, dwarfing the 240 million barrel release during the Russia/Ukraine crisis of 2022.

But barrels in a salt cavern are not barrels on a tanker. Strategic reserves are a stock. What matters to markets is the flow, the rate at which those barrels can be drawn down and delivered. And here the historical data is unambiguous: IEA coordinated releases have never exceeded 2 million barrels per day. The largest single week drawdown during the 2022 release was 8.4 million barrels. Even at the theoretical maximum combined drawdown rate across all G-7 nations, you are looking at roughly 2 million bpd sustained over months.

Now set that against the deficit.

6.2 to 6.7 million barrels per day of production is physically offline as of this writing. Not stuck behind a chokepoint. Not waiting for an insurance backstop or a naval escort. Gone. The facilities are shut down, damaged, or operating under force majeure.

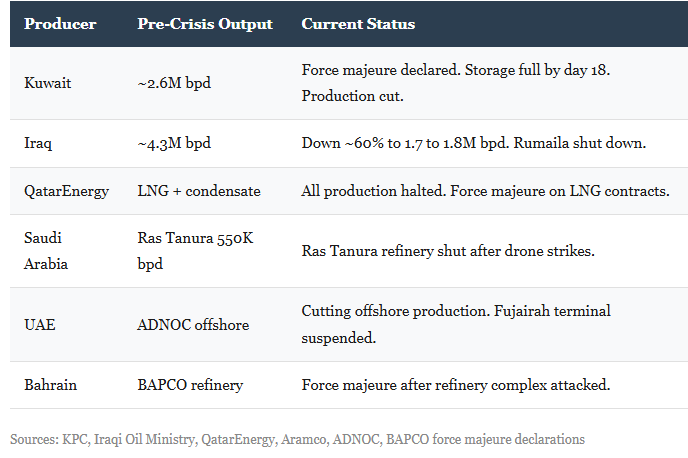

At a release rate of 2M bpd against a production deficit of 6.5M bpd, strategic reserves cover roughly 31% of the shortfall. That is before accounting for the broader net supply impact. 20 million barrels per day was flowing through the Strait of Hormuz before the closure. Saudi Arabia can divert roughly 6 to 7M bpd via the East West Pipeline from Abqaiq to Yanbu on the Red Sea, alleviating that volume from strait dependency. But subtract that workaround and you still have approximately 14M bpd of missing flows with no alternative routing. Kuwait cannot pipeline out. Iraq’s southern exports are landlocked behind the strait. Qatar’s LNG has no bypass infrastructure. UAE’s offshore production has nowhere to go.

At 14M bpd of net missing flows, 400 million barrels covers 28 days even at a theoretical 100% instantaneous release rate, which has never been attempted and is physically impossible given the mechanics of salt cavern extraction, pipeline transfer, and port loading.

The math is simple. At any realistic draw rate, a coordinated release covers a fraction of the shortfall for a limited duration. It does not solve a physical supply crisis. It delays the recognition of one.

The Barrels Are in the Wrong Hemisphere

This is the part that most commentary misses entirely.

The G-7 is the United States, Canada, United Kingdom, France, Germany, Italy, and Japan. Six of seven are Atlantic basin countries. Their strategic reserves are stored accordingly. US SPR barrels sit in four salt cavern sites along the Gulf of Mexico coast in Louisiana and Texas. European reserves are distributed across North Sea and Mediterranean tank farms. Japan maintains roughly 254 days of supply, the most exposed G-7 member, but also the one least likely to drain its own buffer given that it sits directly in the blast radius of the Pacific Asian supply crisis.

The supply deficit is not showing up in the Atlantic basin. It is showing up in Pacific Asia first and hardest because 84% of crude transiting Hormuz goes to Asia. China alone imports nearly 6 million barrels per day through the strait. India, South Korea, Japan, and Taiwan are all massively exposed.

These shipping times assume available tanker capacity, which does not exist. Over 200 crude and product tankers are stranded in the Gulf per Lloyd’s List Intelligence. VLCC spot rates hit $423,736 per day. Clarksons estimates 3,200 ships idle globally due to the conflict. The tanker fleet that would carry released SPR barrels to Asia is the same fleet that is currently unable to move because of the Hormuz closure, war risk insurance withdrawal, and physical danger.

So the proposal amounts to releasing Atlantic basin barrels at Atlantic basin draw rates through Atlantic basin ports onto tankers that don’t exist for delivery to a Pacific basin deficit that is 4 to 6 weeks of sailing time away. By the time SPR barrels from Louisiana reach a refinery in South Korea or eastern China, the crisis will have either resolved itself or metastasized into something strategic reserves cannot address.

Historical Precedent and the 2022 Comparison

The 2022 IEA coordinated release is the obvious reference point, and the comparison actually undercuts the case for action.

In 2022, the IEA released 240 million barrels in response to Russia’s invasion of Ukraine. The US contributed roughly half, drawing the SPR down from approximately 568 million barrels to its eventual low of around 347 million barrels. The release was sustained over six months at an average rate of roughly 1.3 million bpd from all participating countries.

The 2022 release addressed a potential supply disruption. Russian barrels were still flowing throughout the crisis, rerouting to India, China, and Turkey via the shadow fleet. The physical supply loss from sanctions enforcement was never more than 1 to 2 million bpd net, because barrels found alternative buyers. The SPR release was designed to suppress speculative positioning and provide a price ceiling, not to replace physical supply that had disappeared from the market.

The 2026 situation is categorically different. This is not a rerouting problem. This is a physical blockage of the world’s most critical energy chokepoint with simultaneous production shutdowns across multiple Gulf producers. The barrels are not going somewhere else. They are not going anywhere. Kuwait’s wells are being shut in, risking 10% to 30% permanent reservoir damage if the shutdowns extend beyond three to four weeks. QatarEnergy’s LNG trains require weeks of controlled restart procedures even after the all clear. Iraq’s Rumaila, one of the world’s largest fields, is offline.

Releasing strategic reserves into a physical blockage is like using a garden hose on a house fire. The tool exists. It just does not match the scale of the problem.

Probability Assessment: 25% to 35% This Week

The political dynamics make an actual release unlikely in the near term, and virtually impossible at the headline volume.

Only three of seven G-7 countries have expressed support for a coordinated release, per officials cited in the initial reporting. That means four are either opposed, undecided, or hedging. France holds the G-7 presidency this year and their finance minister said publicly that the group is “not there yet” on a collective release after two full days of emergency meetings. When the chair of the process is using language like that, nothing is imminent.

Fatih Birol, the IEA executive director, is actively working against it. He told reporters last Friday that there are “no plans for a collective action at this stage” and described the market as having “plenty of oil,” calling it a “huge surplus.” Birol saying the market is well supplied while Brent trades above $100 is not delusion. It is strategic positioning. He understands that releasing reserves into a crisis with no resolution timeline depletes the IEA’s only emergency tool without fixing the underlying problem. He is preserving ammunition.

The Trump administration has its own reasons for reluctance. This White House spent over a year refilling the SPR after the Biden administration drained it to a 40 year low, successfully rebuilding reserves to approximately 415 million barrels. A major drawdown is a direct political reversal that contradicts the “energy dominance” narrative. Trump himself downplayed the idea over the weekend, saying supplies were ample and prices would fall.

India, the world’s third largest oil consumer and one of the countries most exposed to the Hormuz disruption, has refused to participate. India is an associate member of the IEA, not a full member, and is not obligated to follow IEA directives. Indian officials explicitly stated that those responsible for the war should deal with its consequences. Without non-G-7 participation from major consuming nations, the entire burden of any release falls on Western reserves that are geographically distant from where the crisis is hitting hardest.

Japan is in the most conflicted position. It holds 254 days of supply and has every reason to participate in a coordinated release as the only Asian G-7 member. But it is also the G-7 country most directly threatened by the Pacific Asian supply deficit, which creates an incentive to hoard rather than release. Japan drained reserves during the 2022 release (22.5 million barrels) and understands the replacement cost. The most probable outcome is that Japan releases unilaterally for domestic consumption and perhaps to its closest regional trading partners, not as part of a coordinated IEA action that sends barrels west. That is not a G-7 coordinated release. That is Japan looking after Japan, which is exactly what you would expect from the one G-7 member sitting inside the crisis zone.

My last note

If a release does materialize, I expect it to be smaller than 300 to 400 million barrels, with draw rates capped at historical norms of 1 to 2 million bpd, and the barrels flowing primarily into Atlantic basin refineries. Pacific Asia, where the crisis is most acute, will continue to tighten regardless.

Thanks! Outside of trading the J and K (March & April settlements), an end to the fighting is clearly the only solution. What’s less clear is what happens the day after Trump declares victory and goes home… does Iran retain veto power over the strait alone? Under appreciated complication to the usual TACO.

So they went ahead and Japan also moving faster. All of the points in the piece hold, I just wonder why the IEA got behind it in short order after being sceptical on Monday.

Suspect it's because something is better than nothing, and nothing is whats goanna come out of Hormuz for a while.